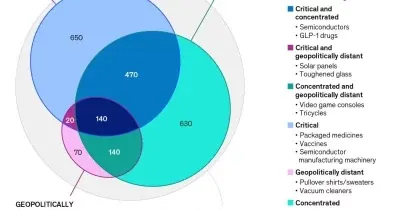

McKinsey: $2 Trillion Needed to Rebuild U.S. Manufacturing Capacity

McKinsey estimates the United States requires $2 trillion in capital investment to restore domestic manufacturing capacity. The scale of required spending could reshape global investment flows, though workforce, energy, and infrastructure constraints remain unresolved.

Key Takeaways

- 1## The Investment Scale McKinsey's analysis estimates $2 trillion in total investment needed to rebuild U.

- 2S.

- 3manufacturing capacity to competitive levels.

- 4The figure encompasses capital expenditure across multiple industrial sectors and infrastructure modernization, according to the consulting firm's report.

- 5## Structural Barriers to Execution Beyond capital availability, the rebuild faces three material constraints.

The Investment Scale

McKinsey's analysis estimates $2 trillion in total investment needed to rebuild U.S. manufacturing capacity to competitive levels. The figure encompasses capital expenditure across multiple industrial sectors and infrastructure modernization, according to the consulting firm's report.

Structural Barriers to Execution

Beyond capital availability, the rebuild faces three material constraints. Workforce capacity—including skilled labor availability and training pipelines—remains underdeveloped in many regions. Energy infrastructure and grid reliability must expand to support relocated or new manufacturing facilities. Transportation and logistics infrastructure requires parallel upgrades to connect production centers to ports and distribution networks.

Implications for Capital Allocation

The scale of capital required could meaningfully reshape investment flows across multiple asset classes and geographies. Private equity, corporate capex budgets, and public infrastructure funding would all need to increase substantially to meet the $2 trillion target. Whether this investment materializes depends partly on policy incentives, tariff structures, and private-sector return expectations—all currently uncertain.

Why It Matters

For Traders

Large infrastructure and manufacturing capex cycles historically lift commodity and industrials sectors; watch for early positioning in steel, semiconductor equipment, and materials stocks.

For Investors

A multi-year $2T rebuild signals sustained demand for capital; infrastructure funds, private equity, and energy plays may benefit from policy-driven growth, though execution risk remains high.

For Builders

Blockchain-based supply chain and logistics protocols may find new use cases if manufacturing reshoring requires transparent tracking across fragmented domestic production networks.