Nansen API Adds Backtesting Data and Faster Top-Ups for Strategy Replay

Nansen released two API enhancements: backtesting data access and accelerated top-up functionality for strategy replay. The updates are designed to streamline algorithmic trading workflows and reduce operational friction for traders validating strategies.

Key Takeaways

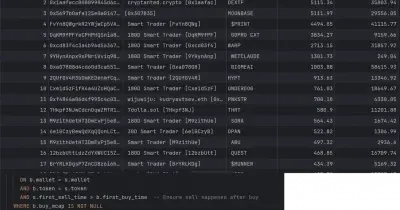

- 1## New Backtesting Data Access Nansen's API now exposes historical backtesting data, allowing traders to validate trading strategies against past market conditions without manually reconstructing datasets.

- 2The feature integrates with Nansen's on-chain analytics infrastructure, enabling algorithm developers to test decision logic against real transaction and price history.

- 3## Faster Top-Up Mechanics The second update accelerates the funding process for strategy replay, reducing the time required to replenish capital between test runs or live trading sessions.

- 4Traders can now trigger top-ups programmatically through the API, cutting manual approval steps that previously slowed iteration cycles.

- 5## Implications for Algorithmic Trading These changes lower the operational overhead for teams running systematic trading strategies.

New Backtesting Data Access

Nansen's API now exposes historical backtesting data, allowing traders to validate trading strategies against past market conditions without manually reconstructing datasets. The feature integrates with Nansen's on-chain analytics infrastructure, enabling algorithm developers to test decision logic against real transaction and price history.

Faster Top-Up Mechanics

The second update accelerates the funding process for strategy replay, reducing the time required to replenish capital between test runs or live trading sessions. Traders can now trigger top-ups programmatically through the API, cutting manual approval steps that previously slowed iteration cycles.

Implications for Algorithmic Trading

These changes lower the operational overhead for teams running systematic trading strategies. Faster feedback loops on backtests and streamlined capital management allow developers to deploy and refine strategies more quickly, though the updates do not alter Nansen's core pricing model or data latency.

Why It Matters

For Traders

Faster backtesting cycles and programmatic top-ups reduce time between strategy ideation and live deployment, compressing iteration speed for quant teams.

For Investors

Nansen's expanding API surface signals a push deeper into the systematic trading workflow, potentially expanding addressable revenue per user but not materially altering market structure.

For Builders

Traders integrating Nansen data into proprietary backtesting frameworks can now source historical snapshots directly, reducing dependency on external data providers for strategy validation.